Gujarat Gas gains 3% as analysts retain bullish view, see double digit-return post Q4

Press Release - Update on Morbi – English

Gujarat Gas Limited (GGL) is the authorized supplier of Piped Natural Gas (PNG) in Morbi. Over the years, GGL has established a comprehensive gas distribution network to serve the entire potential demand of the Morbi ceramic cluster.

Press Release - Update on Morbi – Gujarati

ગુજરાત ગેસ લિમિટેડ (GGL) મોરબીમાં પાઈપ્ડ નેચરલ ગેસ (PNG) પૂરો પાડવા માટેની અધિકૃતતા ધરાવે છે. ગુજરાત ગેસ દ્વારા મોરબી સિરામિક વિસ્તારની ગેસની જરૂરિયાતને સંપૂર્ણત: પૂરી કરી શકે એ માટે વ્યાપક ગેસ નેટવર્ક ઉભું કર્યું છે.

Press Release – Gujarat Gas announces Q3 FY 2025-26 results

CNG volume: Achieved highest volume of 3.45 mmscmd in Q3 FY26, as compared to 3.12 mmscmd to Q3 FY25, increase by 11 %.PNG (Domestic) volume of 0.83 mmscmd in Q3 EY 26 and PNG (CommerCial) volume of 0.17 mmscmd as compared to 0.74 mmscmd and 0.15 mmscmd in Q3 FY25, increase by 11 % and 8% respectively.

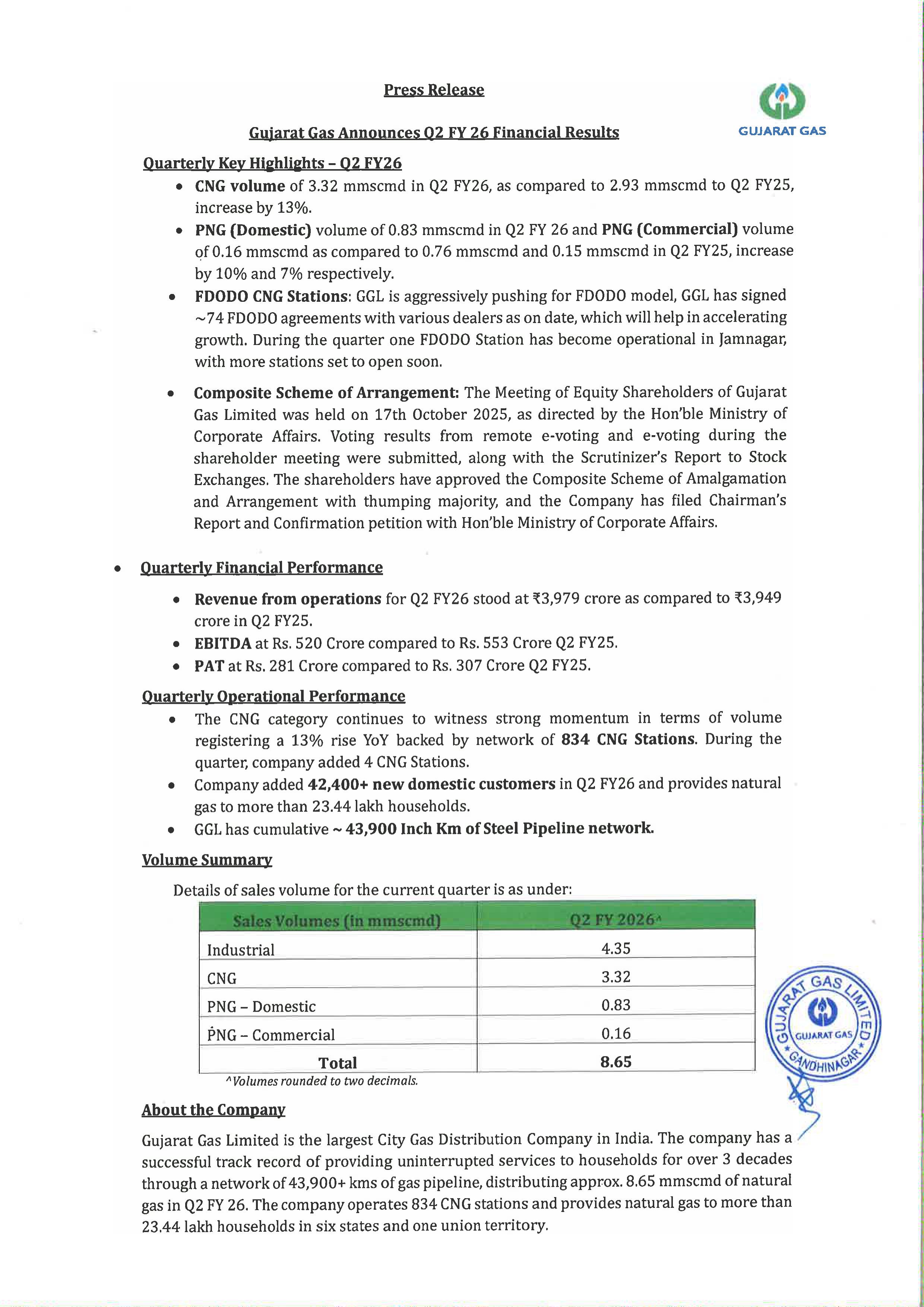

Press Release – Gujarat Gas announces Q2 FY 2025-26 results

CNG volume of 3.32 mmscmd in Q2 FY26, as compared to 2.93 mmscmd to Q2 FY25, increase by 13%. PNG (Domestic) volume of 0.83 mmscmd in Q2 FY 26 and PNG (Commercial) volume of 0.16 mmscmd as compared to 0.76 mmscmd and 0.15 mmscmd in Q2 FY25, increase by 10% and 7% respectively.

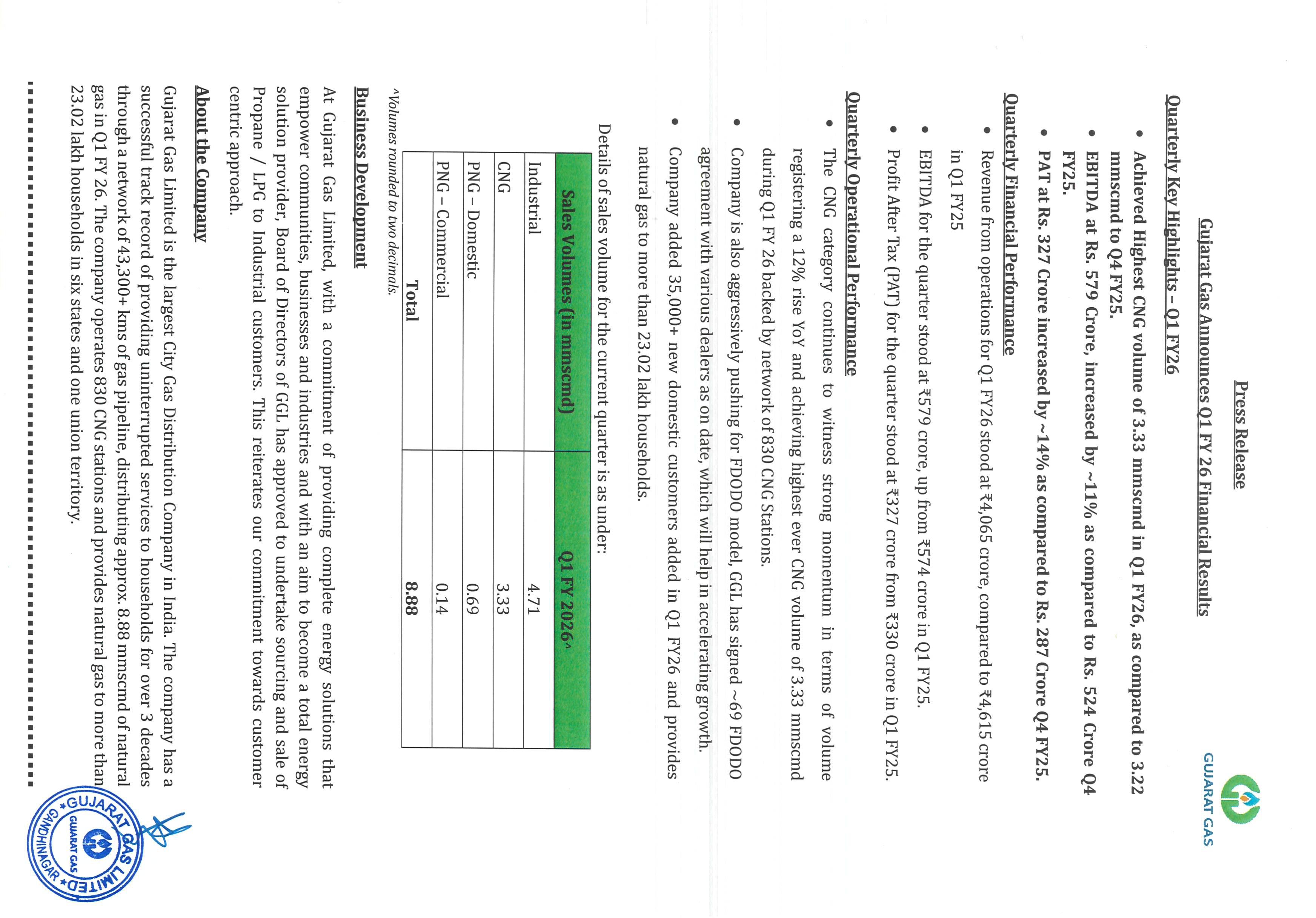

Press Release - Gujarat Gas announces Q1 FY 26 & Annual FY 2025-26

Achieved Highest CNG volume of 3.33 mmscmd in Q1 FY26, as compared to 3.22 mmscmd to Q4 FY25. EBITDA at Rs. 579 Crore, increased by ~11% as compared to Rs. 524 Crore Q4 FY25. PAT at Rs. 327 Crore increased by ~14% as compared to Rs. 287 Crore Q4 FY25

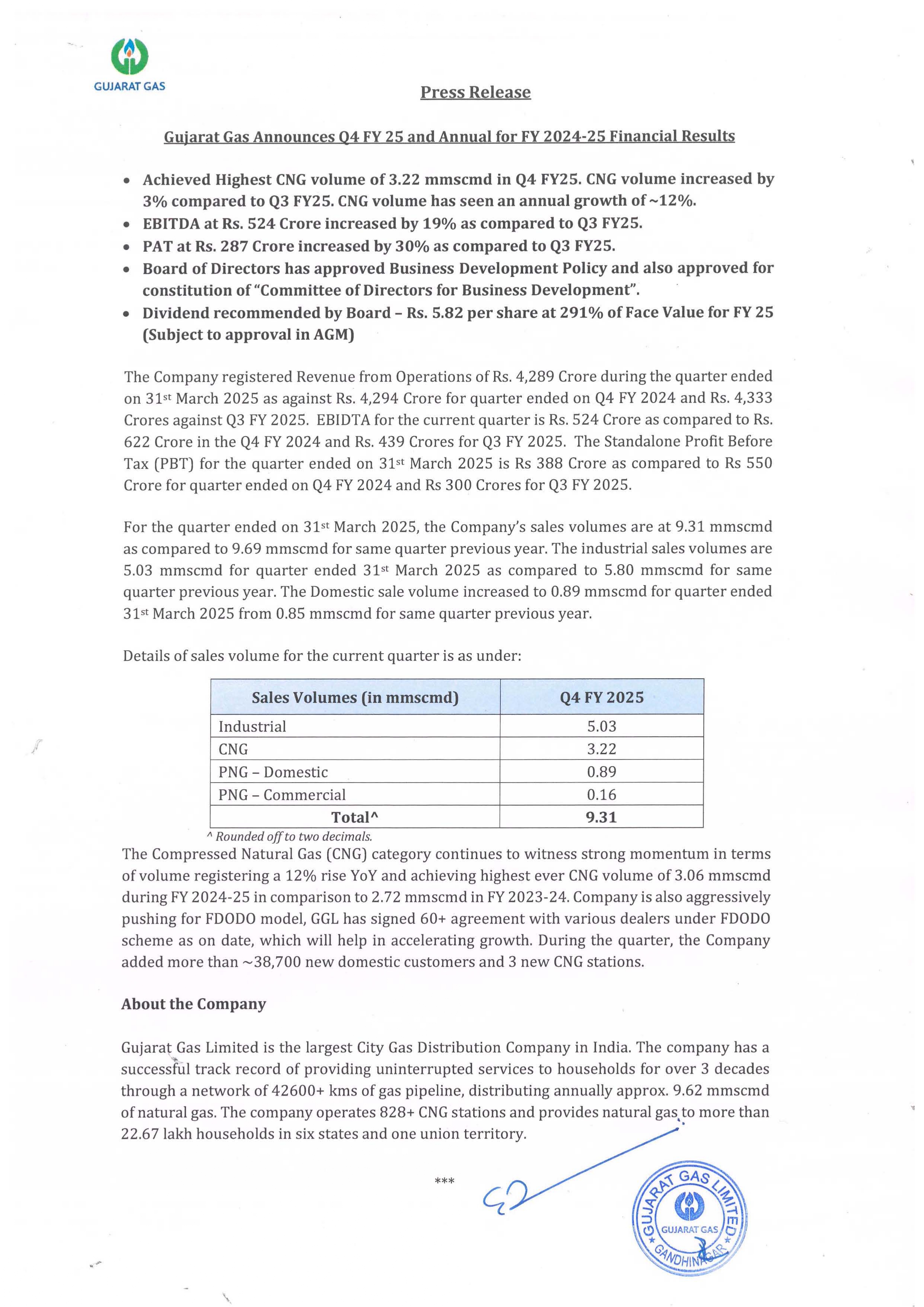

Press Release - Gujarat Gas announces Q4 FY 25 & Annual FY 2024-25

The Company registered Revenue from Operations of Rs. 4,289 Crore during the quarter ended on 31st March 2025 as against Rs. 4,294 Crore for quarter ended on Q4 FY 2024 and Rs. 4,333 Crores against Q3 FY 2025. EBIDTA for the current quarter is Rs. 524 Crore as compared to Rs. 622 Crore in the Q4 FY 2024 and Rs. 439 Crores for Q3 FY 2025. The Standalone Profit Before Tax (PBT) for the quarter ended on 31st March 2025 is Rs 388 Crore as compared to Rs 550 Crore for quarter ended on Q4 FY 2024 and Rs 300 Crores for Q3 FY 2025.

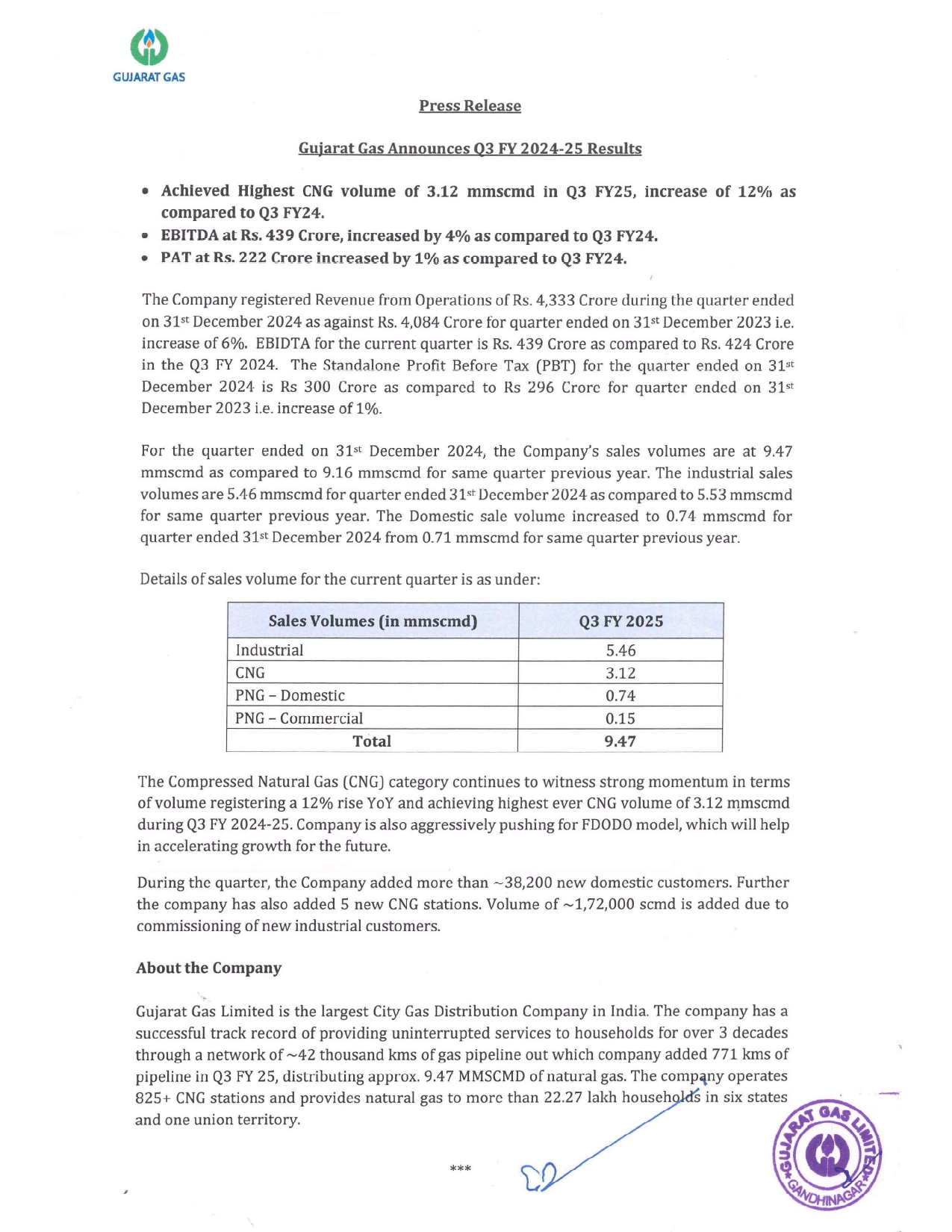

Press Release – Gujarat Gas announces Q3 FY 2024-25 results

The Company registered Revenue from Operations of Rs. 4,333 Crore during the quarter ended on 31st December 2024 as against Rs. 4,084 Crore for quarter ended on 31st December 2023 i.e. increase of 6%. EBIDTA for the current quarter is Rs. 439 Crore as compared to Rs. 424 Crore in the Q3 FY 2024. The Standalone Profit Before Tax (PBT) for the quarter ended on 31st December 2024 is Rs 300 Crore as compared to Rs 296 Crore for quarter ended on 31st December 2023 i.e. increase of 1%.

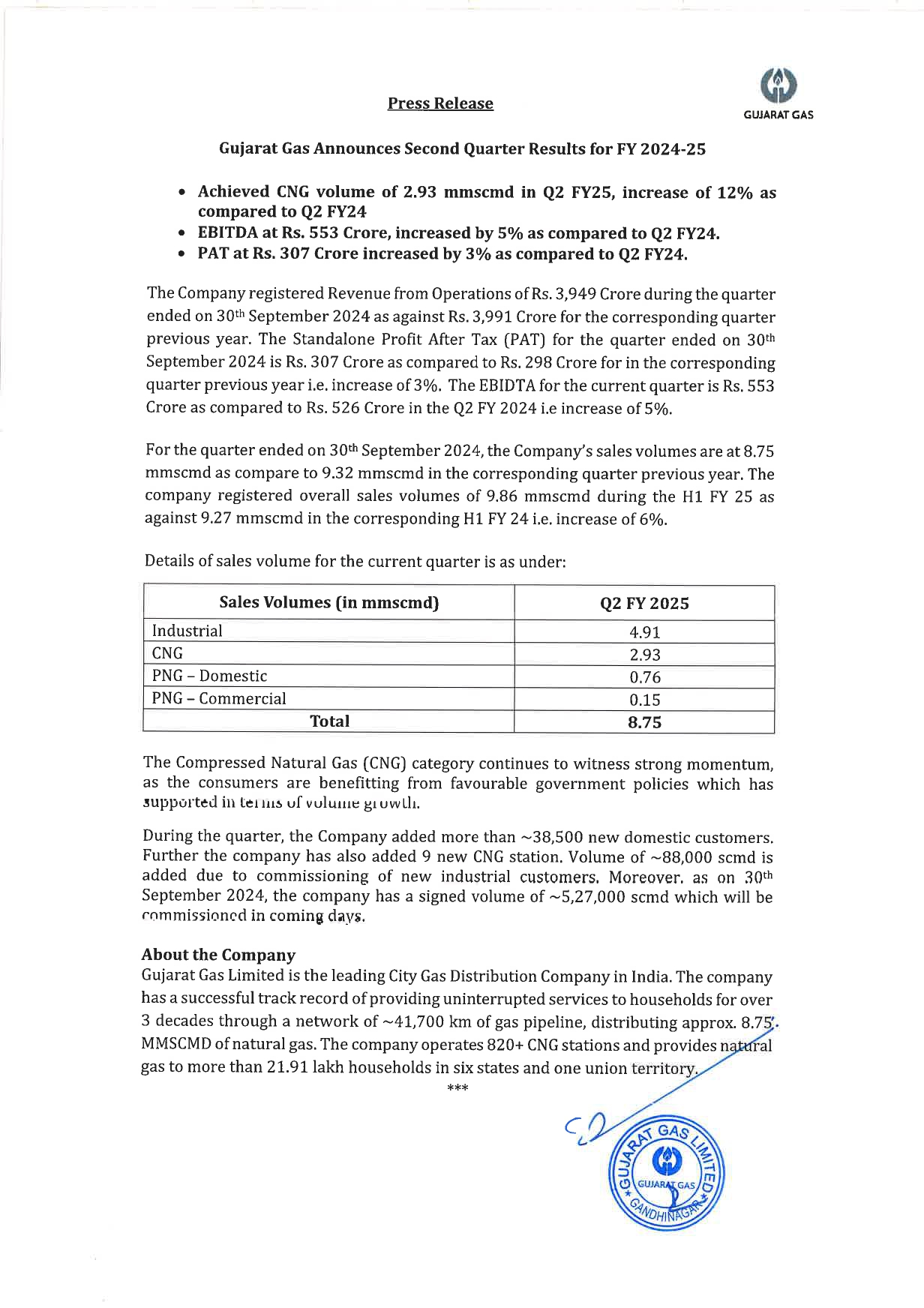

Press Release – Gujarat Gas announces Q2 FY 2024-25 results

The Company registered Revenue from Operations of Rs. 3,949 Crore during the quarter ended on 30th September 2024 as against Rs. 3,991 Crore for the corresponding quarter previous year. The Standalone Profit After Tax (PAT) for the quarter ended on 30th September 2024 is Rs. 307 Crore as compared to Rs. 298 Crore for in the corresponding quarter previous year i.e. increase of 3%. The EBIDTA for the current quarter is Rs. 553 Crore as compared to Rs. 526 Crore in the Q2 FY 2024 i.e increase of 5%.

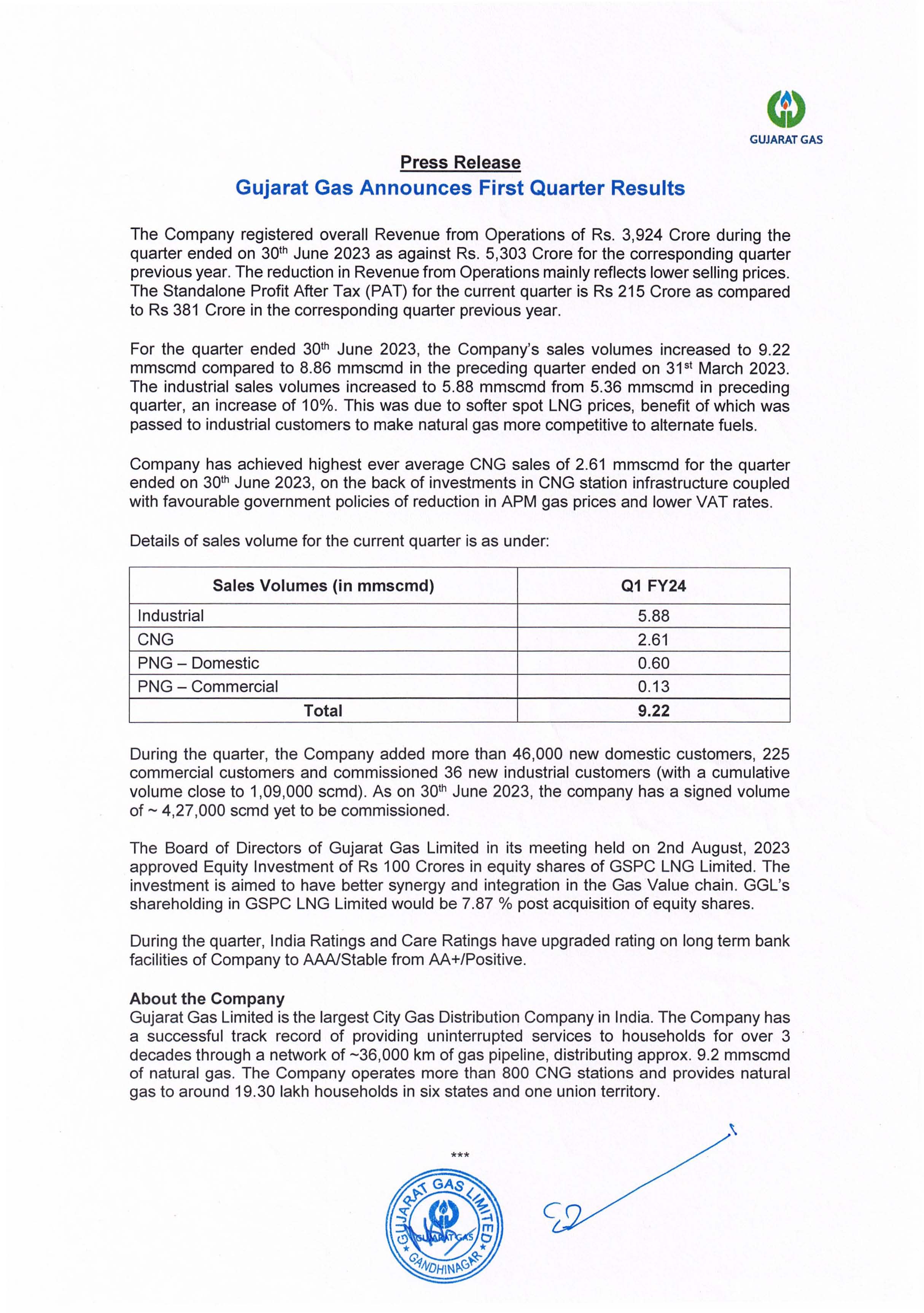

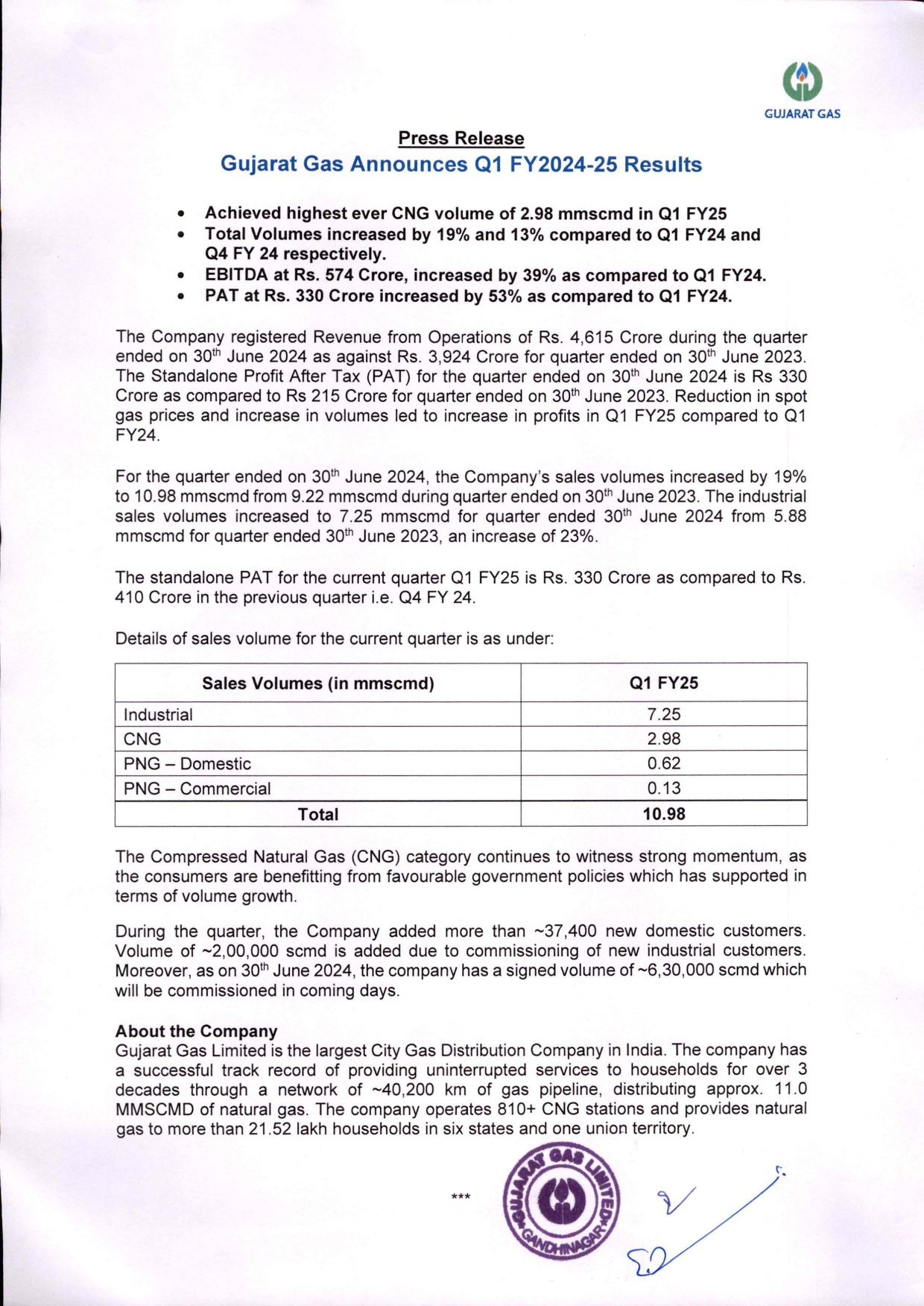

Press Release – Gujarat Gas announces Q1 FY 2024-25 results

The Company registered Revenue from Operations of Rs. 4,615 Crore during the quarter ended on 30th June 2024 as against Rs. 3,924 Crore for quarter ended on 30th June 2023. The Standalone Profit After Tax (PAT) for the quarter ended on 30th June 2024 is Rs 330 Crore as compared to Rs 215 Crore for quarter ended on 30th June 2023. Reduction in spot gas prices and increase in volumes led to increase in profits in Q1 FY25 compared to Q1 FY24.

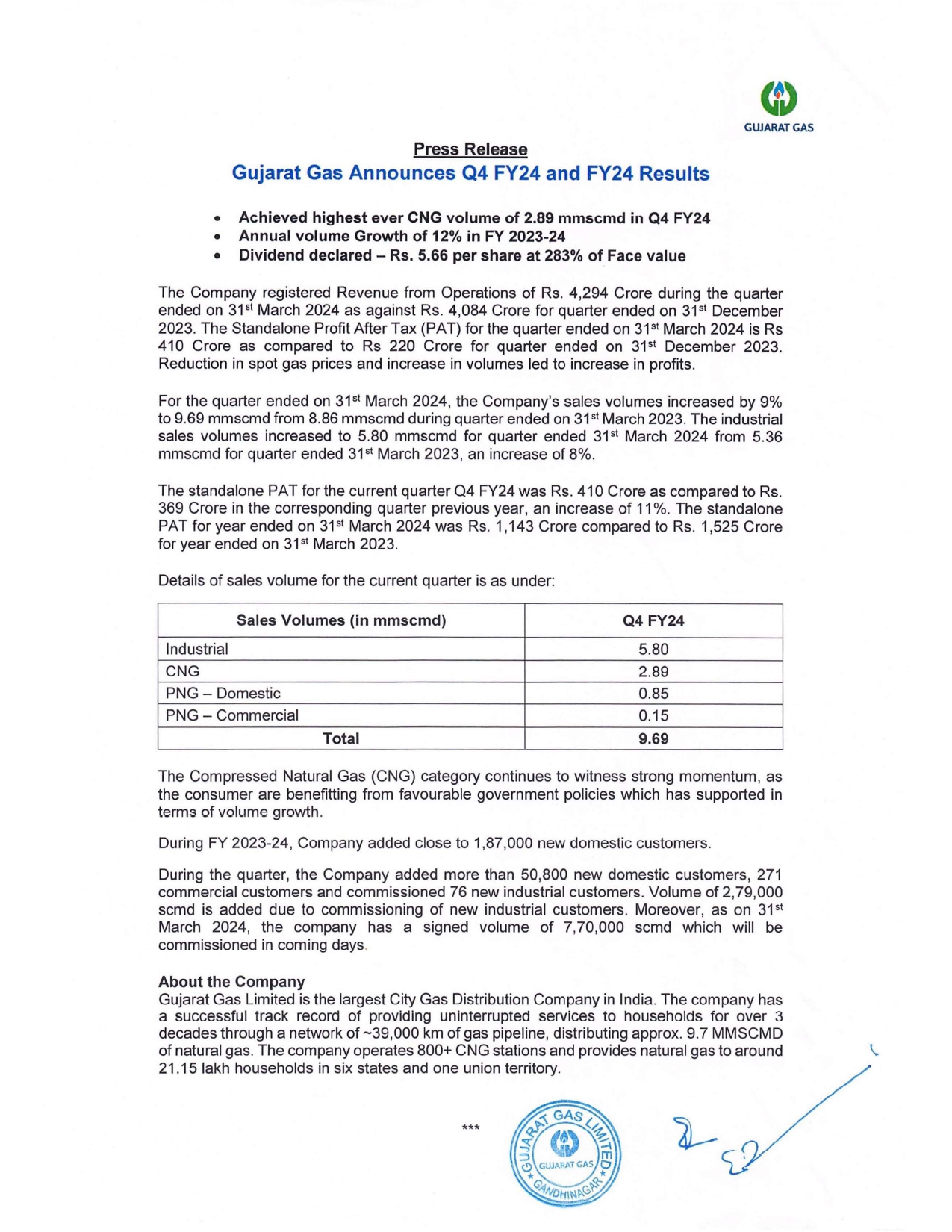

Press Release – Gujarat Gas announces Q4 FY & FY 24 Results

The Company registered Revenue from Operations of Rs. 4,294 Crore during the quarter ended on 31% March 2024 as against Rs. 4,084 Crore for quarter ended on 31st December 2023. The Standalone Profit After Tax (PAT) for the quarter ended on 31 March 2024 is Rs 410 Crore as compared to Rs 220 Crore for quarter ended on 31%! December 2023. Reduction in spot gas prices and increase in volumes led to increase in profits.

Press Release – Gujarat Gas Limited (GGL) offering an Industry first alternate fuel price linked gas pricing

Gujarat Gas Limited (GGL), the largest City Gas Distribution (CGD) Company in India, has always pioneered in providing customer centric solutions over the past 3 decades. Through the innovative solutions, GGL has led from the forefront in making “Natural Gas a preferred fuel for Industrial use”

Press Release – Gujarat Gas Limited invites Expression of Interest (EoI)

Gujarat Gas Limited (GGL), the largest City Gas Distribution (CGD) Company in India, is making rapid strides in the CGD areas by launching an aggressive customer centric campaign. GGL has comprehensively transformed its strategy for industrial segment, with a customer centric vision focusing on customer convenience, awareness, faster response and automation of all processes so as to further penetrate the existing market and get customers on board. With a focus on sustainability, GGL strives to be a key player in the energy transition, contributing to a greener and more sustainable future

Press Release – Gujarat Gas Limited and Bharat Petroleum Corporation Limited sign MoU

In a landmark move aimed at enhancing the accessibility and range of energy solutions for consumers Gujarat Gas Limited (GGL) and Bharat Petroleum Corporation Limited (BPCL) have entered into a Memorandum of Understanding (MOU). This strategic partnership marks a significant milestone in the energy sector, bringing together two leading entities to offer a comprehensive suite of products and services to customers across the state.

Press Note - FDODO Scheme Success

The Board of Directors at Gujarat Gas Limited (GGL) concluded a highly productive meeting on 13th February 2024, where they commended the success of the recently launched "FDODO" scheme for new CNG Stations. The scheme has received massive response, with over 700 online applications submitted by the enthusiastic potential partners.

Press Release - 3rd Qtr Dec. 2023

The Company registered Revenue from Operations of Rs. 4,084 Crore during the quarter ended on 31 st December 2023 as against Rs. 3,991 Crore for quarter ended on 30th September 2023. The Standalone Profit After Tax (PAT) for the current quarter is Rs 220 Crore as compared to Rs 298 Crore for quarter ended on 30th September 2023.

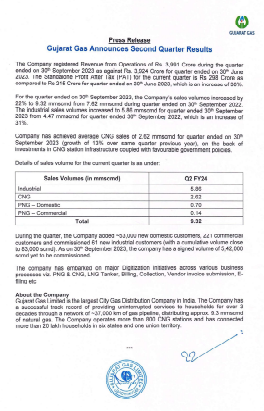

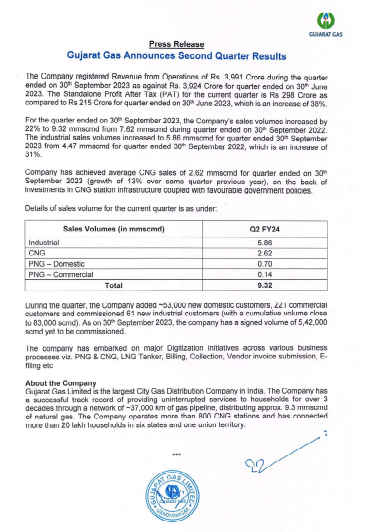

Press Release - 2nd Qtr Sept 2023

The company registered Revenue from Operations of Rs. 3,991 Crore during the quater ended on 30th september 2023 as against Rs. 3,924 Crore for quarter ended on 30th June 2023. The Standalone Profit After Tax (PAT) for the current quarter is Rs 298 Crore as compared to Rs 215 Crore for quarter ended on 30th June 2023, which is an increase of 38%.